When it comes to car insurance, the term “full coverage” often provides a sense of security. However, understanding what happens when your car is totaled under a full coverage policy can be crucial in times of unexpected accidents. In this article, we will explore how full coverage insurance works when your car is totaled, ensuring that you have a clear understanding of what to expect.

Introduction

Car accidents are unexpected events that can leave you in a state of shock. Understanding how your full coverage insurance comes into play when your car is totaled is crucial for a smooth claims process. Let’s break down the complexities and demystify the procedure.

Full Coverage Insurance: What Does it Include?

2.1. Liability Coverage

Full coverage insurance typically includes liability coverage, which pays for damages to other people and their property if you are at fault in an accident. However, it does not cover your car’s damages in this scenario.

2.2. Collision Coverage

Collision coverage, part of full coverage insurance, covers the cost of repairing or replacing your car if it’s damaged in a collision with another vehicle or object, regardless of fault.

2.3. Comprehensive Coverage

Comprehensive coverage, another component of full coverage, covers non-collision-related damages such as theft, vandalism, natural disasters, or hitting an animal.

The Scenario: Your Car Is Totaled

3.1. Determining Total Loss

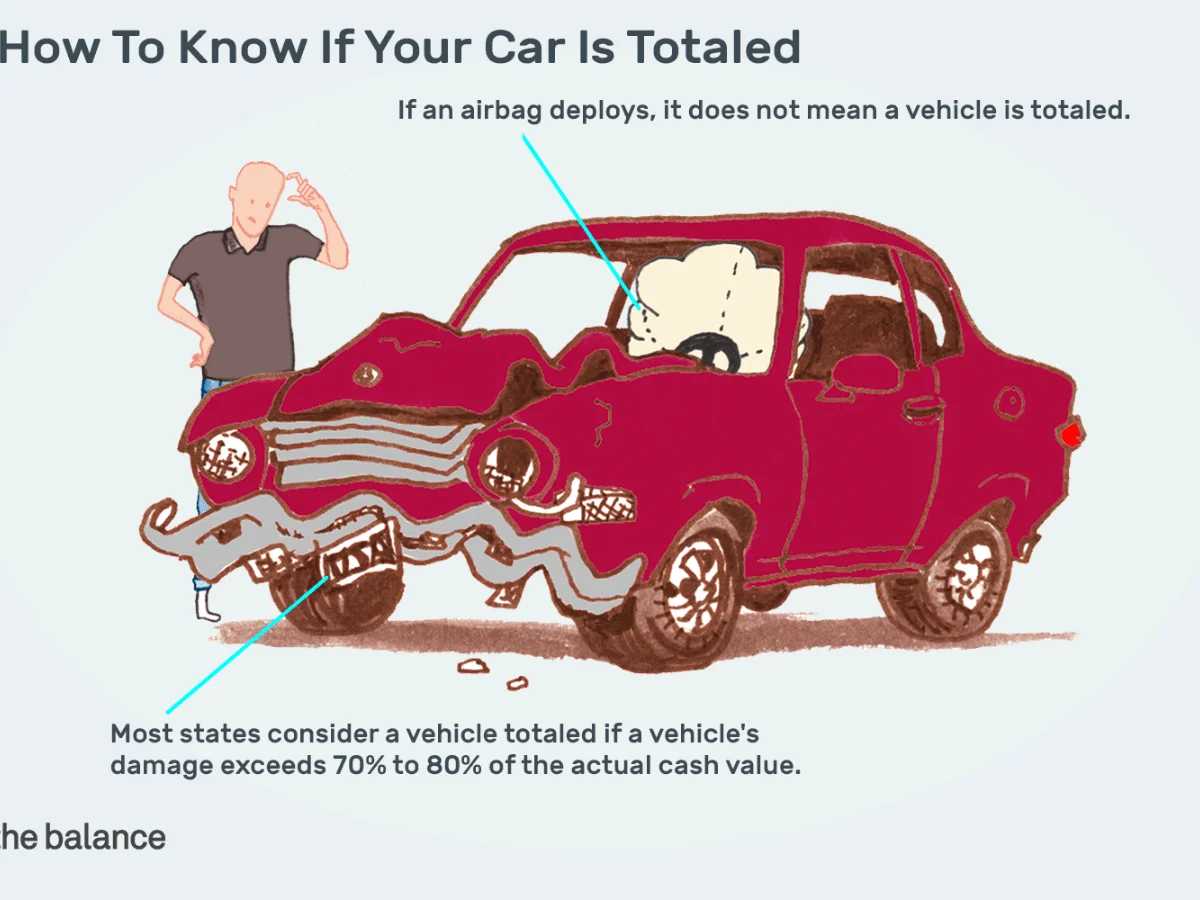

When your car is considered “totaled,” it means the cost of repairing it exceeds its actual cash value (ACV). This determination is typically made by your insurance company’s adjuster.

3.2. The Role of Deductibles

Your insurance deductible, the amount you pay out of pocket before your insurance coverage kicks in, plays a role in the totaled car scenario. Lower deductibles mean less out-of-pocket expenses for you.

The Claims Process

4.1. Reporting the Accident

After your accident, promptly report it to your insurance company. They will guide you through the claims process and provide instructions on the next steps.

4.2. Appraisal and Evaluation

An appraiser will assess the extent of the damage and determine if your car is indeed totaled. They will consider factors such as the car’s age, condition, and market value.

Understanding Payouts

5.1. Actual Cash Value (ACV)

In most cases, your insurance company will provide a payout based on your car’s ACV, which is its market value before the accident minus depreciation. This amount may not cover the full cost of a new vehicle.

5.2. Gap Insurance

Gap insurance is optional but valuable. It covers the difference between your car’s ACV and the amount you owe on your auto loan, ensuring you don’t end up with outstanding debt after a total loss.

What Happens to Your Car?

6.1. Salvage Titles

When a car is totaled, it may receive a “salvage title,” indicating it’s been significantly damaged. Salvage titles can affect a car’s resale value.

6.2. Repairs and Salvage Auctions

Some individuals choose to repair their totaled cars, while others may sell them at salvage auctions. The choice depends on the extent of damage and personal preferences.

Conclusion

In conclusion, full coverage insurance provides substantial protection when your car is totaled, but it may not cover the entire cost of replacing your vehicle. Understanding the claims process, payouts, and optional gap insurance is essential for managing the financial impact of a total loss.

FAQs

8.1. What is the primary difference between full coverage and liability-only insurance?

Full coverage insurance includes liability, collision, and comprehensive coverage, while liability-only insurance covers damages to others but not your own car.

8.2. Can you choose not to repair your totaled car and keep the insurance payout?

Yes, you can opt not to repair your totaled car and keep the insurance payout. This choice can be influenced by various factors, including the extent of damage and personal preferences.

8.3. Does full coverage insurance always cover the full cost of a totaled car?

Full coverage insurance typically covers the actual cash value (ACV) of the totaled car, which may not be the full cost of a new vehicle. Gap insurance can help cover this gap.

8.4. Is gap insurance necessary for all full coverage policies?

Gap insurance is optional but highly recommended, especially if you owe more on your car than its ACV. It ensures you don’t end up with outstanding debt after a total loss.

8.5. How can you ensure you receive a fair payout for your totaled car?

To ensure a fair payout, gather evidence of your car’s condition, maintenance, and any upgrades. You can also seek independent appraisals and negotiate with your insurance company if necessary.

Read More: https://www.rozyjos.com/

More Related:

How to Determine if Your Prescription Is Single Vision or Progressive

Can I Get Single Vision Glasses with a Progressive Prescription?

How to Make Progressive Bill Pay Without Logging In

Understanding and Alleviating Eye Strain with Progressive Lenses

A Clear View: Tackling Blurry Distance Vision with Progressive Lenses